How Top A&E Firms Are Upping Their Cash Flow Game in a Time of Crisis

How Top A&E Firms Are Upping Their Cash Flow Game in a Time of Crisis

A roundtable discussion (long, but meaty)

The COVID-19 pandemic has created new challenges and questions for architecture and engineering firms on how to manage their cash flows in a time of global pandemic and economic downturn. AEC Advisors, an investment banking and corporate finance advisory firm to the architecture and engineering industries, and BST Global, hosted a virtual roundtable on May 1st with a panel of A&E financial leaders to discuss a range of issues around maintaining their firms’ cash position. Below is a condensed and edited version of that conversation.

The panel was moderated by Andrej Avelini, President, AEC Advisors, with participants: Jon Kessler, CFO, Gannett Fleming; Cindy Milrany, CFO and Chief Strategy Officer, Freese and Nichols; Scott Stewart, CEO, IBI Group; and Javier Baldor, Executive VP, BST Global.

Andrej: The first question I want to ask has to do with cash balances. What is an appropriate amount of cash for an AE firm to have? Are there some rules of thumb in terms of how much a firm should have on its balance sheet at any one time?

Jon: Gannett Fleming doesn’t normally have a significant amount of cash on hand. A rule of thumb we use to measure is cash relative to the average monthly operating cash outflow, rather than as a percent of topline. As a rule of thumb, I think 30-60 days of operating cost is adequate. And that’s not just cash on hand, but access to capital- -we have a line of credit, and we don’t keep a lot of cash on hand.

But I think that’s dependent on any firm's client mix as well as future expectations of DSO (days sales outstanding). Our current expectation is that, although it’s good today, we are in the public markets, and we have an expectation that DSO might drag out, so we’ve been working with our banks to extend more on the lines-- not that we’ve drawn on it-- but to extend it because that 30-60 days might not be adequate..

Andrej: And how does that 30-60 days of operating cost translate to a percent of revenue?

Jon: Maybe about 5-8%.

Cindy: We have more than 5% of revenue. I agree with Jon from an operations standpoint. We also keep cash reserves for divestitures as part of our ownership transition model, and that gives us some flexibility if we were to need to borrow from those funds as well.

Andrej: I do think client mix does matter. If you are working with a private sector client or land developer, you’ll need a whole lot more cash right now than if you’re working for a hospital, say, or a public sector client in general. Now let’s talk about how that relates to your line of credit, because I always thought that having 5% of your revenues tied up in cash, earning next to nothing, is inefficient from a return perspective. Especially because you could always go into your line of credit if you need it to manage your cash flow. But what I obviously did not count on is the pandemic, where that line of credit might not be available to you. So, my question to you is threefold:

How often are you talking to your bankers right now, have you pulled down on your line of credit, and are you seeing your banker pull back on your line of credit to say that maybe we’re not as comfortable giving you a full line at this point in time?

Scott: We’re certainly in regular contact with our banks. I wouldn’t say it’s on a daily or weekly basis. It’s more around events and where we see our operating position. And that’s an important conversation to have with them as we update our financials, because our line is driven off of our EBITDA, and we’re anticipating a drop in EBITDA that will affect our ability to draw on the line. As long as we’re within the covenants-- and we do constant updating of our covenants in those conversations, and in those forecasts -- we’re fine. And that ties back to how we manage cash and what we borrow from the bank.

We do a monthly cash forecast that we measure against daily. Cash forecasts are tied against aging receivables, understanding our client base and what their history has been. So, we can anticipate our net cash for the end of month and then reserve against that without having to go into the bank line.

Andrej: Any other thoughts on line of credit. What advice would you give others?

Jon: So I think the last global financial crisis was a banking crisis, which created a lot of banking liquidity issues. You saw a lot of companies grab capital, whether they needed it or not. One of the first things I did when this crisis started was to contact our banking partners to talk to them about their liquidity issues. I also did some research on liquidity on whether that’s an issue and if we should grab up to our line of credit and worry about things later. It doesn’t appear at the moment that it’s an issue, and certainly the Fed has stepped in and made sure there is banking liquidity. So we have not chosen to draw, but as things unfold, that is something we are taking a look at.

Andrej: Do you know what your line is as a percent of revenue?

Jon: It’s right around 10%.

Cindy: We do have a line of credit, and it’s small compared to what Jon is talking about. But again, we have this pool of money for divestitures that we rely on for that excess cash need. We’ve only drawn down on a line of credit twice in my thirty five years at Freese and Nichols.

We are in contact with our bank more than we normally are. Our bank officer has talked to us every week just to be sure that, if we did need money, the amount of our line would not prevent us from getting more than that.

Scott: Our line is about a third of our revenue.

Andrej: I think a reason why fewer people are pulling on their line of credit is because of their PPP loans, at least in the U.S. Our latest survey says that over 90% of firms in this industry of under 500 employees have received the loan. And it’s averaged about 11% of revenues.

Let’s get specific about how we can improve cash flow. I do want to set up a bit of the Why before we get into the How. And I’d like to address the importance of minimizing working capital:

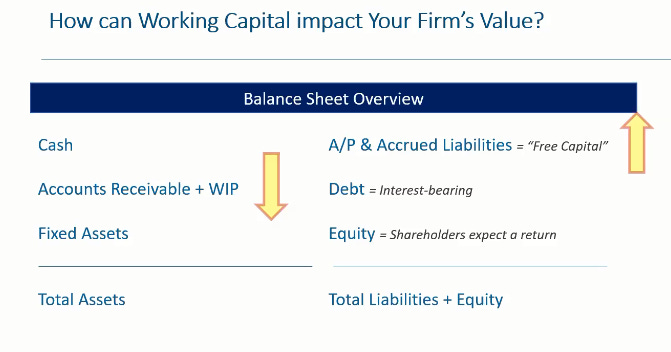

Working Capital Reduction Primer

Andrej: I think now, in this crisis, minimizing working capital could be a crucial differentiator between the ones that skate through it, and the ones that don’t perform so well. So first, let’s define working capital:

Working capital = Accounts Receivables + Work in Process (WIP) - (Accounts Payable + Accrued Liabilities)

When we think about the three ways to finance assets - AP & Accrued Liabilities, Debt and Equity-- we call AP and Accrued Liabilities “free capital” because there is no interest expense. Paying your vendors every 30 days-- not every day-- is a form of free capital. Prepayments from clients are a form of free capital.

AEC Advisors, LLC

So in addition to reducing AR and WIP, the goal on the right side of the balance sheet should be to maximize free capital, minimize debt, and minimize equity so you can get a better return on that equity.

Reducing your working capital with free capital unlocks cash and improves return on equity, which increases the value of your company.

So this is the Why. Let me turn to you guys to address the How.

On the WIP - how do you get WIP out the door. In our survey, only 10% of you are intending to bill faster than you used to, which I thought was a very low percentage. What are some of the things you guys are doing to bill faster?

Jon: At Gannett Fleming, historically, we’ve closed timesheets once every two weeks, which runs with our payroll system. We have now moved to closing time weekly, which will have a dual effect: First, it was originally intended to help project managers more quickly understand time being posted to projects, so that they could help manage projects.

But the secondary aspect is for cash flow. We are looking at the fringes, because for us it will be the fringes where we can bill clients more than once a month, and we expect to do that with the help of closing time weekly. Unfortunately, a majority of our clients will only accept 30-day invoicing. They won’t accept less. But we are going to bill quicker where we can.

Cindy: And we’re in a similar situation to Jon in that most of our clients say that we can’t bill more frequently than 30 days. But where we’ve put the push is at our project manager levels. So, if PMs ask to hold a bill, we are pushing back and there has to be a really good reason. We’re making sure that PMs are billing all the effort, not holding back on things that we could be billing. And, as Jon said, we’re also trying to see if there are a few contracts that we could bill more frequently.

Javier: I remember attending a conference with TetraTech, Dr. (Li-San) Hwang. He said the number one KPI is AR. And how you’re collecting your AR, in effect, tells you about the quality of your work and how happy your customers are. If you’re reluctant to bill, that should tell you something. Is there some underlying reason why you’re not billing, or they are not paying you, which could be related to the service you are delivering? That’s a philosophy about discerning underlying issues sooner.

In addition to philosophy, it also comes down to leadership and discipline. We see firms that are strong on the DSO side and have strong strategies in tracking their collections. A lot of this is just blocking and tackling

Andrej: Let’s talk about how we collect faster. Other than billing faster, are there any other techniques to help with collections. Jon what are you doing to get the bills in faster?

Jon: We rely on project managers and client relationships when it comes to cash collection. There are a number of them that don’t want to upset the client by making calls. We do have to work harder on culture, relating to cash collection. But as Javier said, it’s blocking and tackling. I will get on a call now with the PM to ask: is there a reason why you haven’t sent a bill out? Do you know you have issues with a project? Is there a reason why the client hasn’t paid?

We know that clients use all the excuses to slow down payments. And we’ve got to work our way through those minefields. And it’s just doing those simple things that we are taking more seriously now because, while we haven't seen a degradation of cash flow yet, with our clients, that’s coming. So what I’m concerned about is three, to six, to nine months outs.

Scott: About 6-8 years ago the focus was always on the project manager. When we were a private company, that was great because it was a partnership, and everyone was focused on collecting the money because it directly flowed through to the partners. When we went public, we lost that edge, and relying on the project managers proved to be a challenge, especially as we grew bigger and acquired more firms with different operating practices.

So, starting 6-7 yrs ago we opted to have all of the collections follow-up be on our project accountants as a first order of business, and that has been a central part of how we’ve been able to improve our collections. And the project managers are then able to focus on the execution of the work. PMs are called in when there are problems, and the project directors have oversight of collections in their area of responsibility, and they are certainly measured against performance on collections, so they have their eye on it. But the first line of attack is through the project accountant.

Cindy: About 15-20 years ago we switched from having project managers call on delinquent accounts to having that be part of the accounting function, and it has been a wonderful transition for us. Our project managers love not having to be the ones to make those calls. Sometimes we do have to get the project manager involved, but what we find is the majority of time it can be handled accounting-to-accounting. And some of our government clients have been old fashioned and we’ve seen this as a time to get those clients to move to electronic billing. And then we’ve also gotten a lot of our clients on ACH payments in the last couple of weeks. People who have said they weren’t interested in that before, all of a sudden are.

Jon: We ran a list of all of our clients paying us by mailing us a paper check and we’ve reached out to all of them saying they must pay us by ACH, or by mailing a check to our lockbox.

Andrej: What percentage of your payments is collected through ACH?

Jon:We collect somewhere north of 70%

Cindy: We’re probably less than 50%, but seeing that increase.

Javier: 75%, up from 10% two years ago.

Scott: I’d say it’s under 50% at the moment. But we see this crisis as a great opportunity to change that because it’s an arcane process.

What is your AR DSO? The median seems to be around 90 days for the industry.

Jon: We’re right around 90 days.

Scott: We’re at 68 days. Six years ago, we were at 140. Dropping that working capital has made a huge difference for us. We take pride in that 68 days because it's much better than our peers.

Andrej: That’s definitely the top quartile of your peers, particularly architectural firm peers, who are close to 120 days all in. So you’ve cut it in half. That’s tremendous.

Scott: It might be because we had so many architects and that was a driving factor in having the accounting staff take on that role. Because as you know, architects are more interested in designing buildings and not so much in collecting receivables.

Javier: Cindy and Javier, how about you?

Cindy: We’re probably in the high 60s.

Javier: To be fair, we’re in a different business with different obligations. We’re in the high 20s.

Andrej: Yeah, it’s amazing how bad our industry is when it comes to working capital compared to others. I think we’re the worst.

About 50% of firms have implemented a layoff or furlough already. What measures have you implemented so far and would you recommend to improve cash flow outside of working capital?

Scott: Outside of the obvious - adjusting staff to project requirements and looking at, and, executing both permanent and temporary furloughs-- we’re also adjusting the work week for certain staff in offices where the market is not strong enough at the moment, such as cutting back to four days a week.

We are reviewing our leases -looking at the potential for what a return to work environment might look like with social distancing. It’s almost a trade-off between the work from home benefit and the space required. But we do see in the future, we will be looking to cut back on space by what could be anywhere from 30-40%. And that will be negotiated as leases come available. The change that has taken place with how people work from home is a benefit to the firm. So that’s a top priority for us.

IT is also an absolute priority for us. We invest heavily in it. The benefit that a $12,000 extra cost per month to our IT vendor has yielded to us, is immeasurable in terms of improved engagement and collaboration for all 2,700 IBI staff, and it’s really been spectacular. We see that as the future of the industry and want to be at the forefront of that.

Andrej: I saw in our last survey we asked what percentage of people in your firm had worked from home before versus what you expect it to be after COVID. Before was 5% and after it was 25%. And if you think about lease expenses, they are about 5% of revenue. So, if you could cut that by 25% that would give you a 1% margin on profitability in a 10% margin industry. That could be a big deal. More of a strategic longer-term savings.

Jon: I will echo everything Scott just said as we’re in the same boat. The other thing as it relates to technology is that I expect that the future cost of meetings to drop significantly. We’re already, of course, seeing a huge savings from not flying around the country, particularly for internal meetings. Other things that we could potentially see in terms of immediate cost savings are office fit-outs, where we do have office leases coming up. We’re also taking a look at labor, for sure, to furlough where we can’t utilize people. But we are also taking a look at the must-have employees versus the nice to haves right now.

Javier: I agree with Jon that the overall approach to meetings will change completely. Video conferencing is now widely accepted. Clients are embracing it. So I think there is a big opportunity on the savings side there. On working from home, we’ve seen a lot of support and energy for that. We’ve also seen many that would also love to get back to the office. So, the footprint of real estate will change. What percentage is to be determined, but I think it’s going to be material.

Cindy: We have a really strong backlog. We need the people we have to get the work done. But we’re smart enough to know there are probably some pockets that maybe aren’t as busy as others. So we are using this opportunity to get on board with resource management. With BST it’s called eResource, but all the systems have that. We’ve struggled as a company with that. It’s a cultural thing. About 90% of our backlog is scheduled in eResource and we can really now see where our heavy workload is and where we can shift. We still have a lot of open positions for hiring, and we’re talking to people where their eResource doesn’t support it, then those positions have to go away.

Andrej: What have you learned from this crisis? Will anything change or will you go back to the bad old ways when the crisis passes?

Jon: I think what we’re seeing now is better implementation and execution. What I'm afraid of is If our clients continue to give us work, it will be harder to hold onto the gains that we’ve made. But I do believe we’re going to see more pain down the road than what we’ve seen so far. In which case, I think people will continue to be serious about why driving DSO down and cash flow up is hugely important.

Scott: Never let a good crisis go to waste, and this is an incredible one. There is so much that we have seen as ways to operate including cash management and we have to protect that going forward. Otherwise, if we fall back, and we fall onto hard times, the firms will disappear. It’s going to be essential that we adopt the new practices and procedures, from my mind, all centered around technology, information processes and people.